Managing personal finances has become increasingly complex, especially as more people rely on credit, digital payments, and monthly billing cycles. One concept that often comes up in conversations about financial health is the bills score. While it may sound similar to a credit score, a bills score focuses specifically on how well you manage and pay your regular bills. Understanding your bills score can help you improve your financial stability, qualify for services more easily, and build better money habits over time.

Understanding the Concept of Bills Score

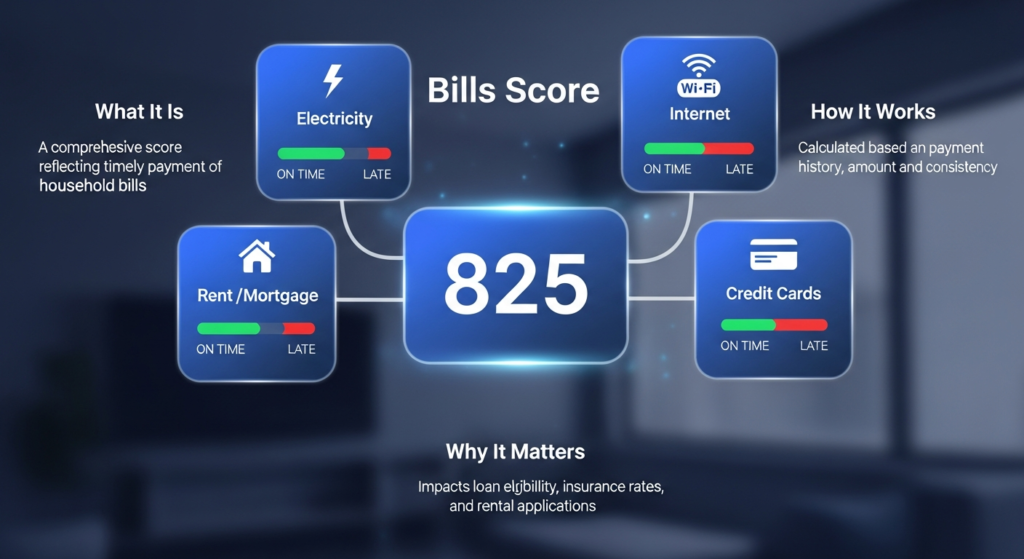

A bills score is a measurement of how consistently and responsibly an individual pays their recurring bills. These bills may include rent, utilities, phone plans, internet services, insurance premiums, and other monthly obligations. Unlike a traditional credit score, which is heavily influenced by loans and credit cards, a bills score centers on everyday financial behavior.

The idea behind the bills score is simple: paying bills on time reflects reliability. Service providers, landlords, and even some employers may use this data to assess whether a person is financially dependable. As more alternative data sources become part of financial evaluations, the bills score is gaining relevance.

How a Bills Score Is Calculated

The calculation of a bills score varies depending on the service or platform tracking it, but the core factors remain similar. Payment history plays the most important role. On-time payments positively impact the score, while late or missed payments reduce it.

Another factor is payment consistency. Someone who pays all bills on time for several years will generally have a higher bills score than someone with irregular payment patterns. The length of payment history also matters, as longer histories provide more reliable data. Some systems may also consider how frequently bills are paid early versus right on the due date.

Bills Score vs Credit Score

Although they are related, a bills score and a credit score are not the same thing. A credit score focuses on borrowed money, such as credit cards, mortgages, and personal loans. It evaluates how much credit you use, how long you’ve had credit accounts, and how well you repay debt.

A bills score, on the other hand, highlights everyday financial responsibility. Many people who lack traditional credit, such as students or individuals new to a country, may still have a strong bills score because they consistently pay rent and utilities on time. This makes the bills score especially valuable for those who are credit invisible or have limited credit history.

Why Bills Score Is Important for Financial Health

A strong bills score indicates financial discipline and stability. It shows that you can manage recurring expenses without falling behind, which is a critical life skill. This can reduce financial stress and help you maintain better control over your budget.

From a broader perspective, a good bills score can open doors. Landlords may feel more confident renting to you, utility companies may waive deposits, and service providers may offer better terms. In some cases, a strong bills score can even support loan or credit applications by supplementing traditional credit data.

Who Uses Bills Score Data

Various organizations rely on bills score data to assess risk and reliability. Landlords often use it when screening tenants, especially when credit scores are low or unavailable. Utility companies and telecom providers may check a bills score before approving service without a deposit.

Financial technology companies also use bills score data to create alternative credit models. These models aim to provide fairer access to financial products by considering real-world payment behavior rather than just borrowing history.

How to Check Your Bills Score

Checking your bills score depends on where it is being tracked. Some financial apps and services offer dashboards that show payment behavior for utilities, rent, and subscriptions. These platforms may calculate a bills score internally or provide insights that closely resemble one.

You can also review your own records by tracking bill due dates, payment confirmations, and bank statements. While this won’t give you a numerical score, it can help you understand your payment habits and identify areas for improvement.

Ways to Improve Your Bills Score

Improving your bills score starts with consistency. Paying all bills on time is the most effective strategy. Setting up automatic payments can reduce the risk of forgetting due dates. Keeping a calendar reminder as a backup is also helpful.

Another approach is simplifying your bills. Consolidating services or aligning due dates can make payments easier to manage. If you anticipate difficulty paying a bill, contacting the service provider early can sometimes prevent late payment reporting and protect your bills score.

Common Mistakes That Lower Bills Score

One common mistake is assuming small bills don’t matter. Even minor late payments can affect your bills score if they occur repeatedly. Ignoring paper bills or email notifications is another frequent issue, especially in a digital-first environment.

Overdrafts and insufficient funds can also indirectly impact your bills score if they cause payments to fail. Maintaining a small buffer in your account can help avoid this problem and keep payments flowing smoothly.

The Future of Bills Score in Personal Finance

As financial systems evolve, the bills score is likely to play a bigger role in financial decision-making. More companies are recognizing that everyday bill payments are a strong indicator of responsibility. This shift could make financial evaluations more inclusive and accurate.

In the future, bills score data may be integrated more deeply into lending platforms, rental applications, and subscription services. This could benefit individuals who manage their bills well but don’t rely heavily on traditional credit.

Conclusion

The bills score is an increasingly important measure of financial reliability that focuses on how well you manage your everyday obligations. By paying bills on time, staying organized, and maintaining consistent payment habits, you can strengthen your bills score and improve your overall financial standing. As alternative financial metrics become more common, understanding and caring for your bills score can give you a meaningful advantage in both personal and professional life.

Frequently Asked Questions (FAQs)

What is a bills score used for?

A bills score is used to evaluate how reliably someone pays recurring bills such as rent and utilities. It can help landlords, service providers, and financial companies assess risk.

Is a bills score the same as a credit score?

No, a bills score focuses on bill payment behavior, while a credit score focuses on loans and credit card usage. They measure different aspects of financial responsibility.

Can paying rent improve my bills score?

Yes, consistently paying rent on time is one of the strongest contributors to a positive bills score.

How long does it take to build a good bills score?

Building a strong bills score can take several months of consistent on-time payments, though longer histories generally lead to better scores.

Can a low bills score be fixed?

Yes, improving payment habits, setting up automatic payments, and avoiding late fees can gradually raise a low bills score over time.